Put Options Lesson 11: Wheat Put Anthology

- Wright team

- May 14

- 3 min read

Very few people understand the relationship between the price change of a futures contract and the resulting price change of its options. For the past ten weeks, we explained how the daily price change of the 2022 September CBOT wheat futures contract impacted the value of its $9.00 and $10.00 put options. Now that we have explained the option vocabulary, the concept of options on futures contracts and a detailed day by day explanation of price action, now we will accelerate the process and explain five days of futures price changes and two of its options.

28 April 2022

September wheat futures contract was down 5¢ today, so all puts should have increased in value. The $10 put settled at 51 5/8, up 2 1/8¢. The $9.00 put settled at 20¼, up 2¾¢.

Today, a September wheat futures hedge made $250, the $10 put made $106.25, and the $9 put made $137.50. Normally, because the $10 put is a dollar closer than the $9 to being in-the-money, the $10 put should have increased in value several cents more than the $9 put, but nothing is 100% in this business.

29 April

The September CBOT wheat futures price was down 15¾¢ today. A futures hedge made $787.50. The $10 September put premium increased 10¢, which is $500. The $9 September put premium increased 5¢, which is $250. About how much did the value of the cash wheat growing in the field change? Since cash wheat is hedged on the futures, cash wheat is worth about 16¢ less today than yesterday. But, the HTA or short futures position gained the about 16¢ to offset the value lost on the cash wheat in the field. That is the definition of a hedge: The loss in one market is offset by a gain in a different market.

May 2

September wheat futures settled unchanged today at $10.58¼. Therefore, the intrinsic (aka in-the-money) value of all the September options was unchanged. What about the time value?

The options lost one day of life, so the probability of the options increasing in value is a bit less as well as volatility continues to calm down, further reducing the time value. The $10 put settled at 60¾ cents, down 7/8ths of cent. The $9.00 put settled at 25¼¢, unchanged.

May 3

September wheat futures settled at $10.49½ today, down 8¾¢. All puts should have increased in value since the futures price was lower. The $10 put gained 1 3/8ths¢ while the $9.00 put gain just an eighth of cent as another day of time was value lost. A short futures short position made $437.50 today, the $10 put made $87.50 and the $9 put gained $6.25. The wheat in the field or bin lost about $437.50, because the cash price = futures plus or minus basis.

May 4

September wheat futures settled at $10.79¼ today, up 29¾¢. All puts should have lost value since the futures price was sharply higher. The $10 put lost 9¾¢ while the $9.00 put was unchanged at 25 3/8¢. A short futures short position lost $1,487.50, the $10 put lost $487.50 and the $9 put lost nothing. The wheat in the field or bin gained about $1,487.50, because cash price = futures plus or minus basis. Note the $9.00 put was so far out of the money ($1.49) before yesterday’s trading began, what does another 29¾ cents make? Obviously not enough to change the price of the $9 put.

It is unusual for futures price to move 30¢ and an option value does not change, but it happens. There is not a direct correlation between futures price change and option price change.

Yes, we have the delta, but that is computer generated number as to what the price correlation should be between options and futures. But options are traded bid and ask, just like the futures and farm auctions. Sometimes, the auction price makes no sense.

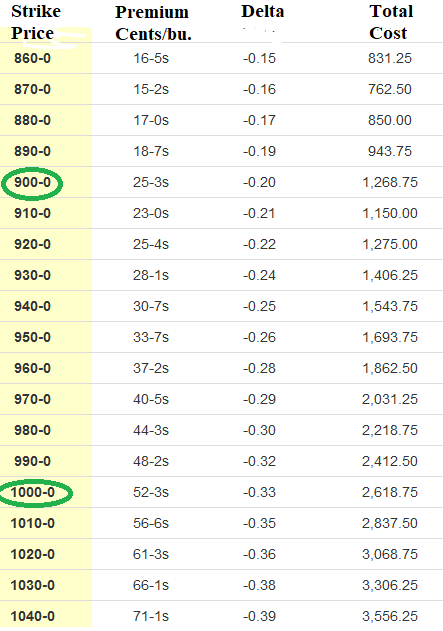

Here are the option prices after today’s action:

Comments