Market Commentary for 10/16/22

- Jon Scheve

- Oct 16, 2022

- 2 min read

Jon Scheve with weekly market commentary made on October, 14, 2022

Following are the highlights of this week’s USDA report that provided more information on the US grain supply.

Corn

While the USDA decreased the average national yield, most of the country’s best corn areas still need to be harvested. Right now, it is uncertain if yields in the east that have not been harvested will make up for the disappointing yields in the west that have been picked.

Considering the value of US corn compared to the rest of the world, it seems reasonable that the USDA decreased export demand. However, their feed estimate is almost 7% lower than the last 4-year average, which may be too low. While the trade still believes exports could decrease a few more bushels, the feed category may have room to offset further export reductions.

The chart below shows current USDA estimates with several different demand scenarios (highlighted in blue) and a range of potential outcomes to the carryout.

Based on the different demand scenarios, the stocks to use ratios could be range bound between last year’s levels and lower levels similar to the 2020 crop, when futures rallied above $8 to ration demand. It seems the USDA is indicating corn demand should remain strong for the rest of the season, which might mean upside price potential is stronger than downside risk for the next several months.

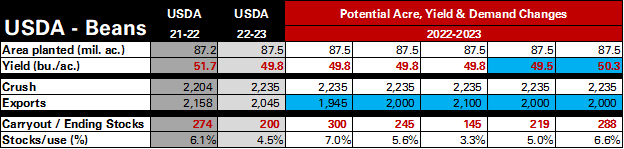

Beans

Based upon information from growers I spoke with the past few weeks, it seemed likely the USDA could decrease the national average yield. I suspect the lower-than-expected yields in the west and inconsistent yields in areas previously considered high potential were the main reasons for the reduction.

Moving forward, bean price direction will be completely dependent on Chinese demand and South America’s weather. The USDA’s total bean export levels are currently below the latest 4-year average in years that did not include the trade war. Plus, it seems the USDA and the trade think Brazil will grow a massive record crop this upcoming season. However, this will only happen if there are no weather issues in the Southern Hemisphere. Next year will be the third year that La Nina will be present, which increases the chances of weather problems. Any perceived issues with growing conditions could cause volatile price swings.

The chart below provides several scenarios based on different supply and demand outcomes (highlighted in blue) to the US crop.

Due to the yield decreases, the possible carryout numbers are not as cumbersome as expected prior to the report. Export demand is key, and it will be watched very closely by the market. While limited export demand could push prices lower, even a minor demand increase would likely spark a rally to help ration demand. Bottomline Moving forward demand for US crops will be driving market direction as well as South American weather. Any potential crop loss in the Southern Hemisphere may mean increased demand for US supply and higher prices to ration demand.

Jon Scheve Superior Feed Ingredients, LLC

9358 Oak Ave Waconia, MN 55387 jon@superiorfeed.com

Comments