Market Commentary for 7/16/22

- Jon Scheve

- Jul 16, 2022

- 4 min read

Jon Scheve with weekly market commentary made on July, 15, 2022

Recession fears continue to plague the market, preventing any major buying by the funds. While weather forecasts are changing daily, the latest USDA national yield estimate of 177 could still be achieved. However, if widespread extreme heat continues with little rainfall over the next two weeks, the national yield average may decrease by 1 or 2 bushels, which would likely mean upside potential in the corn market.

Market Action

Last week I explained how I rolled my July sold futures positions to the May contract and collected 48 cents. This was made with a basis trade at the same time. Following provides some historical context on why I made the basis trade and the final outcome.

During the first few weeks of the Ukraine war the market was very nervous. Traders and risk managers started making trades that covered their needs, anticipating worst case scenarios.

Initially, there was a lot of panic and fear, so the market went into “buy everything” mode. Wheat was the first commodity to really take off. End users began moving their bids against the May contract to the July, September, or even the December contracts for immediate shipment, because the May contract was climbing much faster than later months. This meant cash values were not climbing as fast as futures. No one knew what would happen next because sellers were unsure if they should continue to hold grain or sell immediately and, buyers wondered how they should hedge the grain they were purchasing. There was concern this uncertainty would carry over into the corn market too.

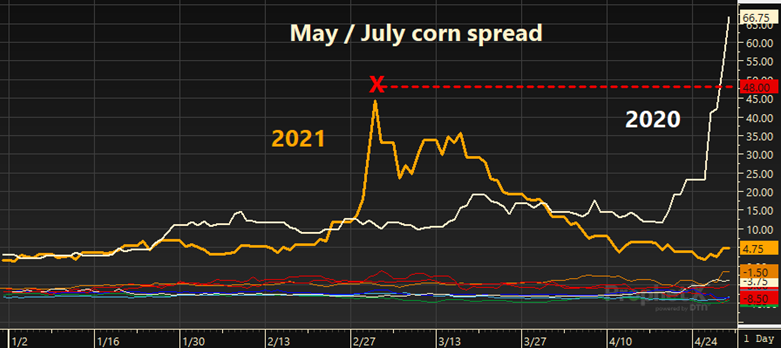

Seven trading days after the war started May corn futures went from $6.80 to $7.80. From February 28th to March 3rd, corn futures spreads between the May and July contracts widened from a 12-cent inverse (i.e., May was 12 cents higher than the July contract) to a 50-cent inverse.

Early on the morning of March 3rd, I noticed grain buyers in the eastern corn belt moved their basis bids to the July contract. I figured it was only a matter of hours before western corn belt grain buyers did the same.

Therefore, I set my basis with one end user for the best delivery time value they had posted. That ended up being the April/May shipment period against the May futures. This shipment time period was higher than the March shipment period shown in the chart below by the yellow X. I made the trade on 70% of my 2021 corn production.

The chart above shows the posted spot March shipment period bids, with freight rates from my farm subtracted from the price, from several nearby end users. When all freight rates were considered, several buyers were basically bidding the same price to me. The basis at my local end users did drop at the close of trading on March 3rd as seen in the chart above and continued to drop over the next 2 weeks by another 30 cents. Since this basis trade was set against May futures, all my hedges in the July futures contract needed to be rolled back to the May contract. This enabled me to also capture additional profit on the huge market inverse of 48 cents represented by the green arrows in the chart above. This meant the basis value I sold for corn picked up on my farm for -10 on May futures was like trading +38 on the July futures picked up on my farm. This type of level would equate to the best basis value I have EVER sold, or even seen available to me for my farm, including the drought crop years of 2011 and 2012. I could have chosen to not set basis and just rolled the July contract back to the May futures and hoped the spread would eventually collapse and then look to roll the spreads again back to the July and set basis in June. However, many in the trade told me they expected the spread to go to levels substantially higher than where it was trading much like the year before (see in the first chart). I was concerned the basis would drop more than any gain I may get from trading the spread. That’s why I wanted to minimize my risk by moving any grain with futures sales against it, at values that I knew at the time were the best ever. Another 10% of my production also had a futures price objective hit against the May contract right after the invasion. I set the basis on those bushels at the same time but was not able to capture the spread trade premium since those sales were not ever in the July contract. This basis trade cleaned up the ’21 crop short positions in my hedge account and left me with 20% of my production unpriced on both futures and basis. At the time I was unsure what to expect from the markets with the first war in Europe in over 80 years. I felt the best risk management plan was to avoid guessing what the spreads, basis or futures were going to do from that point forward during a time of war. I moved to the sideline and waited for more information. Next week I will share what I did with the last 20% of my grain in the bin.

Jon Scheve Superior Feed Ingredients, LLC

9358 Oak Ave Waconia, MN 55387 jon@superiorfeed.com

Comments